Direct Equity vs Mutual Funds: Choose the Work, Risk and Control You Can Sustain

Riya and Kunal had the same long-term goal, but very different ideas about how to invest for it.

Kunal wanted to select individual companies because he valued control. Riya preferred an equity mutual fund because she did not want their household plan to depend on their ability to study and monitor every company.

Neither route is automatically better. The real choice is about who will do the research, how concentrated the portfolio may become, what costs and behaviour risks the investor can manage, and whether the process can be sustained through a full market cycle.

Both Routes Take Equity-Market Risk

Buying shares directly gives the investor ownership exposure to selected listed companies. An equity mutual fund pools investors' money and invests under a stated scheme mandate.

Both can rise or fall with equity markets. A mutual fund is not a capital-guaranteed substitute for shares, and direct ownership does not make a company predictable.

The distinction is mainly in the investment process:

- Direct equity: the investor selects, sizes, monitors and exits individual holdings.

- Equity mutual fund: the investor selects a scheme and delegates security selection and portfolio operations to the fund-management process, while continuing to monitor suitability, costs and performance against the stated objective.

Direct Equity Requires a Repeatable Research Process

Direct equity offers control over what is owned, how much is allocated and when a position is changed. That control is useful only when it is supported by a disciplined process.

SEBI's due-diligence guidance for investors includes understanding the business model, comparing competitors, examining economic conditions, reviewing financial statements, following corporate announcements and considering valuation. This is continuing work, not a one-time stock-screen result.

A direct-equity investor should be able to answer:

- What does the business do, and how does it make money?

- What could permanently weaken earnings, cash flow or governance?

- Why is the current valuation reasonable for the expected risk?

- How much of the total portfolio can be exposed to one company or sector?

- What evidence would change the original investment case?

- Can the investor act on that evidence without panic, attachment or social-media influence?

If these questions are not reviewed consistently, “control” can become unmanaged concentration.

What an Equity Mutual Fund Changes

An equity mutual fund can make diversification and day-to-day portfolio administration easier for an investor. It does not remove the need to choose carefully.

The investor still has to assess:

- the scheme's investment objective and category;

- where it invests and how concentrated it is;

- the Risk-o-meter and other scheme risks;

- expense ratio, exit load and tracking or management approach;

- whether the scheme overlaps with other holdings; and

- whether the time horizon and risk capacity fit equity exposure.

AMFI describes its website as a source for mutual-fund services and information. Investors should use AMFI's official information portal and scheme documents rather than relying only on rankings, advertisements or recent returns.

Direct Equity and Mutual Funds Compared

| Decision factor | Direct equity | Equity mutual fund |

|---|---|---|

| Security selection | The investor chooses each company and position size. | The portfolio follows the scheme mandate and fund-management process. |

| Diversification | Depends on available capital, portfolio construction and investor discipline. | Usually available through a pooled portfolio, but concentration still varies by scheme. |

| Research workload | High and continuous: company, sector, valuation, governance and portfolio monitoring. | Focused on scheme selection, suitability, costs, portfolio characteristics and periodic review. |

| Control | High control over holdings, position size and transaction timing. | The investor controls scheme choice and cash flows, not each security-level decision. |

| Costs | Brokerage, statutory charges, taxes and the cost of research tools or time may apply. | Expense ratio, applicable exit load, transaction-related portfolio costs and taxes may affect outcomes. |

| Behaviour risk | Stock attachment, overconfidence, tips, excessive trading and averaging without evidence. | Chasing recent winners, owning overlapping schemes and stopping investments after market falls. |

| Operational requirement | Trading and demat arrangements through regulated intermediaries, plus secure account practices. | KYC, folio or demat records, nomination and scheme-level transaction documentation. |

NSE explains that investors use registered stock brokers to transact on an exchange. Review its account-opening information for investors and capital-market investor education material. SEBI also advises investors to protect trading and investment account credentials, including never sharing passwords.

Growing SIP Use Does Not Decide Your Choice

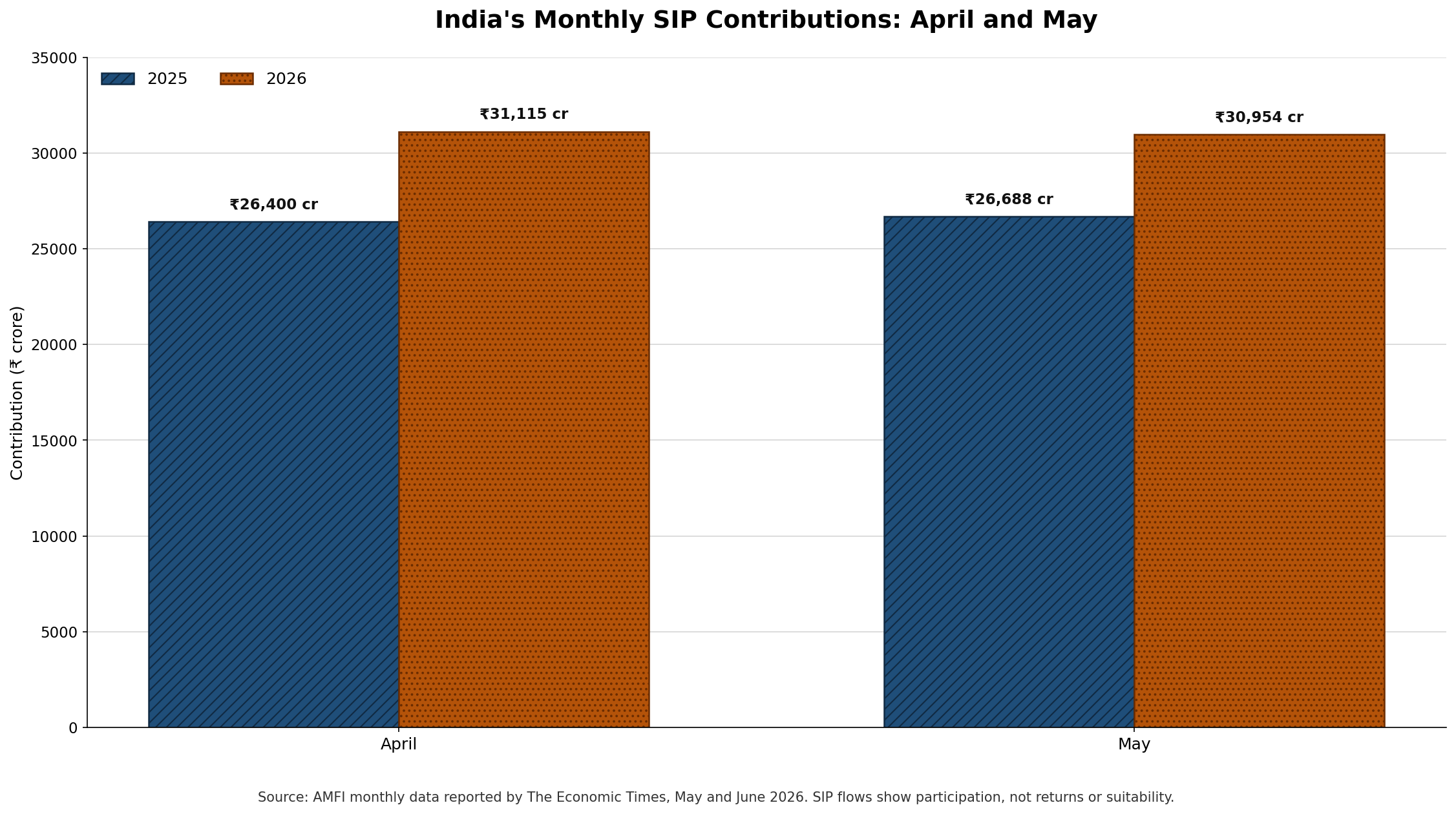

AMFI monthly data reported by The Economic Times showed:

| Month | 2025 | 2026 |

|---|---|---|

| April | ₹26,400 crore | ₹31,115 crore |

| May | ₹26,688 crore | ₹30,954 crore |

The April 2026 figure was about 18% higher than April 2025, while May 2026 was about 16% higher than May 2025. The chart shows growing use of a structured mutual-fund contribution route. It does not show investment returns, lower risk, better scheme selection or suitability for any individual.

Popularity is not a substitute for due diligence.

A Core-and-Satellite Approach Can Separate Two Jobs

Some experienced investors separate the two jobs:

- a diversified fund allocation forms the core of long-term equity exposure; and

- a smaller direct-equity allocation is used only where the investor has the time, skill and documented process to research companies.

This is a planning framework, not a standard allocation recommendation. The suitable mix could be all mutual funds, all direct equity, a combination, or no equity for money that cannot tolerate market loss. The decision depends on goals, time horizon, liquidity needs, risk capacity, knowledge and behaviour.

The image shows the principle without prescribing a percentage: keep the broad, repeatable process central; keep research-intensive decisions limited to what can actually be monitored.

Who May Prefer Direct Equity?

Direct equity may be considered by an investor who:

- understands financial statements, business quality, valuation and governance;

- can diversify without turning the portfolio into an unmonitored collection;

- has time to track material developments;

- uses a written investment case and exit discipline;

- can accept being wrong without doubling down emotionally; and

- does not depend on tips, influencers or unregistered advice.

Control without process is not an advantage.

Who May Prefer an Equity Mutual Fund?

An equity mutual fund may be considered by an investor who:

- wants equity exposure without selecting every company;

- values a pooled, mandate-based portfolio;

- can evaluate scheme category, objective, risk and costs;

- wants a repeatable contribution and review process; and

- accepts that professional management does not assure returns or prevent losses.

Delegation does not remove responsibility. The investor still chooses the scheme and decides whether it remains suitable.

Common Mistakes

- Treating a few successful stock picks as proof of lasting skill.

- Buying too many direct stocks without understanding any of them deeply.

- Holding one sector because recent returns look strong.

- Assuming every mutual fund is diversified, low risk or suitable.

- Selecting schemes only from star ratings or one-year performance.

- Ignoring expense ratio, exit load, brokerage, taxes and turnover.

- Mixing emergency money with long-term equity.

- Sharing trading passwords, OTPs or account access.

- Acting on social-media tips or unregistered advice.

- Comparing a hand-picked winning stock with an entire diversified fund after the outcome is known.

Investor Checklist

Before choosing direct equity, an equity mutual fund or a combination, write down:

- the goal and earliest date the money may be needed;

- the loss the household can absorb without abandoning the plan;

- the hours available each month for research and review;

- the maximum acceptable company and sector concentration;

- the evidence required before buying, holding or exiting;

- all product, transaction and tax costs;

- nomination, account-security and documentation arrangements; and

- a review schedule that does not depend on daily market noise.

For account-opening and investment-service information, review Abhipra Services or visit Abhipra eKYC.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- SEBI Investor guidance on investment due diligence

- SEBI Investor guidance on securing investment accounts

- NSE account-opening information for investors

- NSE capital-market investor education material

- AMFI official mutual-fund information portal

- April 2026 SIP contribution data reported from AMFI by The Economic Times

- May 2026 SIP contribution data reported from AMFI by The Economic Times

Disclaimer

This article is for educational and informational purposes only. It is not investment, trading, legal or tax advice and does not recommend any stock, mutual-fund scheme or allocation. Direct equity and mutual fund investments are subject to market risk, including possible loss of capital. Read all relevant disclosures and scheme-related documents, use regulated intermediaries, and evaluate suitability before investing. Past performance does not indicate future returns. Consult a qualified adviser where appropriate.