NPS Tax Benefits in FY 2026-27: What Changes Between the Old and New Tax Regimes?

Ananya and Vivek both contributed to the National Pension System, but their tax outcomes were different.

Ananya used the old tax regime and made a personal Tier I contribution. Vivek used the new tax regime, where his employer's NPS contribution mattered more than his personal contribution for deduction purposes.

The lesson is simple: “NPS gives a tax benefit” is incomplete unless you identify the tax regime, contributor, account tier and applicable limit.

The Three NPS Tax Sections Do Different Jobs

The current NPS Trust tax-benefits guidance, updated June 16, 2026, separates NPS deductions into three main provisions:

- Section 80CCD(1): deduction for an individual's own eligible Tier I contribution, within the overall Section 80CCE limit.

- Section 80CCD(1B): an additional deduction of up to ₹50,000 for an eligible own Tier I contribution.

- Section 80CCD(2): deduction for an eligible employer contribution to the employee's Tier I account.

These provisions are not interchangeable. A payroll contribution by an employer is not the same as an employee's personal contribution.

Old Tax Regime: Personal NPS Contributions Can Matter

Under the old tax regime, an eligible individual may claim:

- under Section 80CCD(1), up to 10% of salary for an employee or up to 20% of gross total income for a self-employed person, within the combined ₹1.5 lakh Section 80CCE ceiling; and

- under Section 80CCD(1B), an additional deduction up to ₹50,000, subject to applicable conditions.

The Section 80CCE ceiling is important. If an investor has already used the ₹1.5 lakh limit through other eligible deductions, the personal NPS contribution under Section 80CCD(1) may not create an additional deduction. Section 80CCD(1B) is the separate NPS-specific deduction that may still be relevant.

A deduction reduces eligible taxable income. It is not a guaranteed refund or a return from NPS.

New Tax Regime: Focus on Employer Contribution

The personal deductions under Sections 80CCD(1) and 80CCD(1B) are not available under the new tax regime.

However, an eligible employer contribution under Section 80CCD(2) can remain deductible. NPS Trust currently states:

- under the old tax regime, the employer-contribution limit is 14% of salary for Central Government employees and 10% for other employees; and

- under the new tax regime, the limit is 14% of salary for employees, subject to applicable tax and payroll conditions.

For this purpose, salary generally refers to basic salary plus dearness allowance where the terms of employment include it, not the employee's entire cost-to-company figure.

Old Versus New Regime at a Glance

| Contribution route | Old tax regime | New tax regime |

|---|---|---|

| Own Tier I contribution: Section 80CCD(1) | Available subject to the percentage limit and combined ₹1.5 lakh Section 80CCE ceiling. | Not available. |

| Additional own contribution: Section 80CCD(1B) | Additional deduction up to ₹50,000, subject to eligibility and contribution. | Not available. |

| Employer contribution: Section 80CCD(2) | Up to 14% of salary for Central Government employees and 10% for other employees. | Up to 14% of salary for employees, subject to applicable conditions. |

| Tier II contribution | The NPS Trust tax page states that Tier II contributions do not receive these NPS tax benefits. | No corresponding personal NPS deduction. |

Do not select a tax regime from this table alone. The correct comparison must include total income, all deductions, applicable rates, surcharge and cess, payroll structure and other household tax considerations.

Ask Payroll What the Employer Is Actually Contributing

Employer NPS is not created merely by making a personal contribution after receiving salary. It normally requires an eligible employer contribution through the payroll and NPS process.

Ask HR or payroll:

- Does the employer offer NPS under Section 80CCD(2)?

- Is the contribution additional to salary or part of the existing compensation structure?

- Which salary components are used for the percentage calculation?

- How will the contribution appear in payroll records, Form 16 and the NPS statement?

- Are other employer retirement contributions relevant to the applicable aggregate tax limits?

The visual shows the distinction: the employee and employer contribution routes are reviewed separately before both enter the long-term retirement plan.

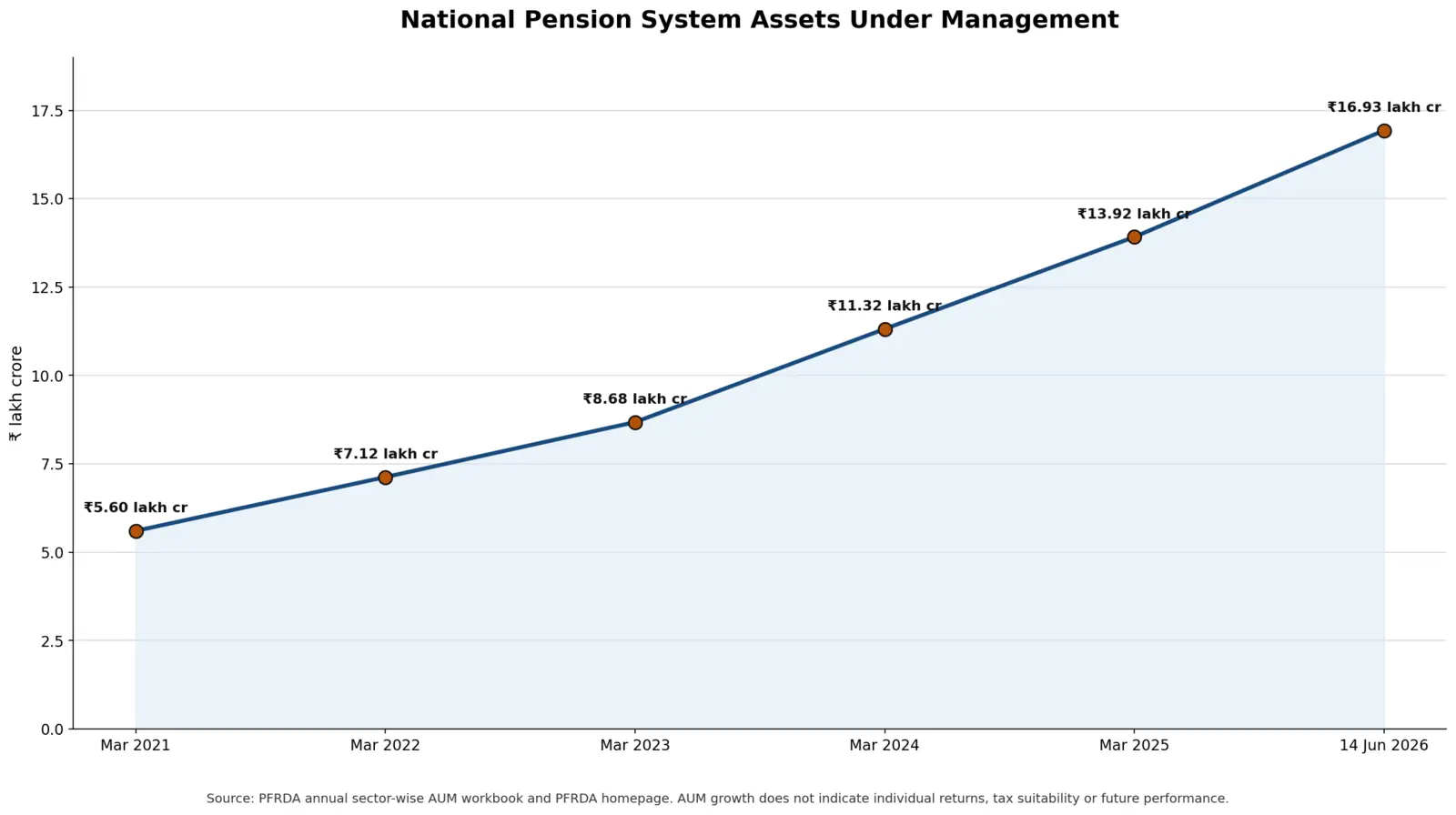

NPS Has Grown, but Scale Does Not Decide Suitability

PFRDA's annual sector-wise data and current homepage statistics show the scale of the National Pension System:

| Reporting date | NPS assets under management |

|---|---|

| March 2021 | ₹5.60 lakh crore |

| March 2022 | ₹7.12 lakh crore |

| March 2023 | ₹8.68 lakh crore |

| March 2024 | ₹11.32 lakh crore |

| March 2025 | ₹13.92 lakh crore |

| June 14, 2026 | ₹16.93 lakh crore |

The system's AUM has more than tripled over this period. That does not show an individual's return, future performance, tax saving or suitability. NPS remains market-linked, and outcomes depend on contributions, asset allocation, charges, market performance and applicable rules.

Withdrawal Tax Treatment Is Not the Same as Easy Liquidity

NPS Trust currently states:

- eligible partial withdrawals can receive tax exemption up to 25% of the subscriber's own contributions, subject to NPS rules and specified conditions;

- the amount used to purchase an annuity at eligible exit is not taxed at the time of purchase;

- annuity income received later is taxable according to the recipient's applicable tax treatment; and

- up to 60% of the corpus withdrawn as an eligible lump sum at normal exit can be tax-exempt.

Tax exemption does not make NPS an on-demand savings account. Current exit and partial-withdrawal rules must be reviewed separately. A percentage permitted under an exit rule should not automatically be assumed to have identical tax treatment.

Common Tax-Planning Mistakes

- Claiming Sections 80CCD(1) or 80CCD(1B) while using the new tax regime.

- Forgetting that Section 80CCD(1) shares the ₹1.5 lakh Section 80CCE ceiling.

- Treating the ₹50,000 Section 80CCD(1B) limit as a guaranteed tax refund.

- Confusing employer contribution with a personal NPS deposit.

- Calculating the employer percentage on total cost to company without checking the statutory salary definition.

- Expecting Tier II contributions to receive the same deductions as Tier I.

- Choosing NPS only for tax without understanding market risk and restricted access.

- Assuming every permitted exit amount is automatically tax-exempt.

- Relying on an old article instead of current tax and PFRDA guidance.

A Practical FY 2026-27 Checklist

Before contributing or restructuring salary:

- Confirm which tax regime applies to the financial year.

- Separate personal Tier I and employer Tier I contributions.

- Check how much of the Section 80CCE ceiling is already used.

- Confirm payroll eligibility and the employer-contribution calculation.

- Verify that contributions appear in NPS and tax records.

- Review NPS liquidity, exit and annuity implications.

- Compare tax outcomes without ignoring the retirement objective.

- Obtain professional tax advice where the payroll or income situation is material.

For service details, visit Abhipra NPS & Pension. Eligible investors can use the online NPS account-opening journey or review the NPS SIP facility. For account-service assistance, contact the Abhipra NPS Desk.

Reviewed by Abhipra Research / Compliance Team.

Source Links

- NPS Trust: Tax benefits under NPS

- PFRDA: About the National Pension System

- PFRDA statistical data and downloadable workbooks

- PFRDA homepage with current NPS statistics

Disclaimer

This article is for educational and informational purposes only and is based on sources reviewed on June 22, 2026. It is not investment, tax, legal, payroll or retirement-planning advice. NPS is market-linked and subject to applicable PFRDA rules, tax law, contribution limits, charges and withdrawal conditions. Tax treatment depends on the investor's regime, income, employment, contribution route and prevailing law. Consult a qualified tax or financial adviser before acting.